Using a free mortgage calculator is an essential tool for anyone considering a home purchase or refinancing. It provides a clear estimate of monthly payments, helping borrowers understand how factors like loan amount, interest rate, and term length impact their finances.

By experimenting with different scenarios, users can determine affordability, compare loan options, and plan their budgets effectively. This empowers informed decision-making, ensuring individuals choose a mortgage that aligns with their financial goals and avoids potential over-extension. Overall, our free mortgage calculator is a valuable resource for simplifying complex calculations and promoting financial confidence.

Understanding Mortgage Calculators and Their Importance

When purchasing a home, one of the most crucial steps is understanding how much you will need to pay each month. A mortgage estimator or home loan mortgage calculator can help you make informed financial decisions by providing accurate estimates of your monthly payments.

Easily Estimate Your Home Loan Payments

![]()

Whether you’re a first-time homebuyer or refinancing your existing mortgage, our free mortgage calculator simplifies the process of computing your payment obligations.

What is a Mortgage Calculator?

- Please use our free mortgage calculator to your right in the sidebar. Choose your details and watch the magic…

A mortgage payment calculator is an online tool designed to help you compute mortgage payment amounts based on various financial factors. These include the loan amount, interest rate, loan term, and property taxes. Using a mtg calculator, you can determine how much house you can afford, compare different loan options, and plan for future expenses.

How a Mortgage Price Calculator Works

Our mtg calc uses the following variables to help figure mortgage payment amounts:

- Loan Amount – The total amount borrowed from a lender.

- Interest Rate – The annual percentage rate (APR) on the loan.

- Loan Term – The number of years you will take to repay the loan.

- Property Taxes – The annual taxes levied on your property.

- Insurance Costs – Homeowners insurance and private mortgage insurance (PMI), if applicable.

- Down Payment – The initial amount you pay upfront to reduce the loan balance.

By entering these values into our home loan calculator, you can quickly determine mortgage payment obligations and plan your budget accordingly.

Benefits of Using a Mortgage Payment Calculator

A mortgage estimator provides several advantages to prospective homebuyers and existing homeowners:

- Budget Planning – Get a realistic view of your monthly expenses.

- Loan Comparison – Compare different loan terms and interest rates.

- Early Payoff Planning – Determine how extra payments can reduce interest costs.

- VA Loan Calculations – Specialized calculations for military service members using a VA home loan calculator.

- Refinancing Analysis – Check how refinancing can lower payments.

How to Use a Mortgage Calculator Effectively

To get the most accurate results from a mtg payment calculator, follow these steps:

- Enter Loan Details – Input the loan amount, interest rate, and term.

- Include Taxes and Insurance – Add property tax rates and insurance costs.

- Adjust Down Payment – Experiment with different down payment amounts.

- Analyze the Results – Review the estimated monthly payments.

- Compare Different Scenarios – Adjust variables to see how they impact payments.

VA Loan Mortgage Calculator for Military Members

For veterans and active-duty service members, our VA mortgage calculator helps determine mortgage payment obligations based on VA loan benefits. The VA loan calculator considers:

- No Down Payment Requirement – VA loans often require no down payment.

- Lower Interest Rates – VA-backed loans typically have competitive rates.

- No PMI – VA loans do not require private mortgage insurance.

- VA Funding Fees – One-time fees associated with VA loans.

Using a VA loan payment calculator, service members can explore affordable housing options while maximizing their VA benefits.

Housing Loan Calculator for Different Loan Types

Different loan programs come with varying terms, rates, and requirements. Our housing loan calculator can assist in evaluating:

- Conventional Loans – Fixed and adjustable-rate mortgage options.

- FHA Loans – Government-backed loans with lower credit score requirements.

- VA Loans – Special loans for military personnel.

- Jumbo Loans – Loans exceeding conventional loan limits.

- USDA Loans – Loans for rural property buyers.

Why Choose Our Free Mortgage Calculator?

Our free mortgage calculator is designed to provide fast, accurate, and user-friendly calculations. Unlike other tools, our mtg calculator is:

- Completely Free – No hidden fees or subscriptions.

- Easy to Use – Simple interface with clear inputs and results.

- Comprehensive – Includes all necessary variables for precise estimates.

- Mobile-Friendly – Accessible on smartphones and tablets.

A home loan mortgage calculator is an essential tool for anyone planning to buy a home, refinance, or compare mortgage options. By using our mortgage price calculator, you can confidently figure mortgage payment obligations and make well-informed financial decisions. Try our free mortgage calculator today to compute mortgage payment details and take control of your home-buying journey!

If you are an investor, please check out this post: Stock Market vs Real Estate Investing.

VA Loan Benefits: A Comprehensive Overview

1. No Down Payment Required

-

Zero Down Payment: One of the most significant benefits is that VA loans can be obtained with no down payment at all, making homeownership more accessible for those who might not have saved for a traditional down payment.

2. Competitive Interest Rates

-

Lower Rates: VA loans typically offer competitive interest rates compared to conventional loans, which can save borrowers thousands over the life of the loan.

3. No Private Mortgage Insurance (PMI)

-

PMI Waiver: Unlike conventional loans where PMI is required if the down payment is less than 20%, VA loans do not require PMI, reducing monthly payments significantly.

4. Flexible Credit Guidelines

-

More Lenient Credit Requirements: VA loans can be more forgiving when it comes to credit scores. While lenders have their own standards, the VA itself does not set a minimum credit score, allowing more people to qualify.

5. No Prepayment Penalties

-

Pay Off Early: VA loans allow borrowers to pay off their mortgage early without any penalties, which can be advantageous if you come into extra money or want to reduce interest over time.

6. Funding Fee Flexibility

-

Funding Fee: While there’s a funding fee that helps keep the VA loan program running, this fee can be financed into the loan amount or waived under certain conditions like receiving a disability compensation from the VA for a service-connected disability.

7. Assumable Loans

-

Loan Assumption: VA loans are assumable, meaning if you sell your home, under certain conditions, the buyer can take over your existing VA loan, potentially at a lower interest rate than current market rates.

8. Streamlined Refinancing

-

IRRRL – Interest Rate Reduction Refinance Loan: Also known as a VA streamline refinance, this allows for quick refinancing with reduced paperwork if you’re looking to lower your interest rate or change from an adjustable to a fixed rate.

VA Loan Benefits: A Comprehensive Overview

VA loans, backed by the U.S. Department of Veterans Affairs, offer numerous advantages specifically for veterans, active-duty service members, and certain members of the National Guard and Reserve. Here are the key benefits of VA loans:

1. No Down Payment Required

Zero Down Payment: One of the most significant benefits is that VA loans can be obtained with no down payment at all, making home ownership more accessible for those who might not have saved for a traditional down payment.

2. Competitive Interest Rates

Lower Rates: VA loans typically offer competitive interest rates compared to conventional loans, which can save borrowers thousands over the life of the loan.

3. No Private Mortgage Insurance (PMI)

PMI Waiver: Unlike conventional loans where PMI is required if the down payment is less than 20%, VA loans do not require PMI, reducing monthly payments significantly.

4. Flexible Credit Guidelines

More Lenient Credit Requirements: VA loans can be more forgiving when it comes to credit scores. While lenders have their own standards, the VA itself does not set a minimum credit score, allowing more people to qualify.

5. No Prepayment Penalties

Pay Off Early: VA loans allow borrowers to pay off their mortgage early without any penalties, which can be advantageous if you come into extra money or want to reduce interest over time.

6. Funding Fee Flexibility

Funding Fee: While there’s a funding fee that helps keep the VA loan program running, this fee can be financed into the loan amount or waived under certain conditions like receiving a disability compensation from the VA for a service-connected disability.

7. Assumable Loans

Loan Assumption: VA loans are assumable, meaning if you sell your home, under certain conditions, the buyer can take over your existing VA loan, potentially at a lower interest rate than current market rates.

8. Streamlined Refinancing

IRRRL – Interest Rate Reduction Refinance Loan: Also known as a VA streamline refinance, this allows for quick refinancing with reduced paperwork if you’re looking to lower your interest rate or change from an adjustable to a fixed rate.

9. Cash-Out Refinancing

Access Equity: VA loans allow for cash-out refinancing, where you can tap into your home equity for home improvements, debt consolidation, or other financial needs.

10. Forbearance and Assistance

Support During Hardships: The VA offers various programs to help borrowers facing financial difficulties, including forbearance options which might not be as readily available or favorable with conventional loans.

11. Property Eligibility

Broad Property Types: VA loans can finance primary residences which include single-family homes, condos, manufactured homes, and even multi-unit properties where one unit is owner-occupied.

12. Loan Limits

No Set Loan Limits: While there are VA loan limits that can affect the amount of the loan the VA will guarantee, there’s technically no maximum loan amount if you have full entitlement, allowing for purchases in high-cost areas.

13. Seller Concessions

Seller-Paid Closing Costs: Sellers can pay all of a veteran’s loan-related closing costs and up to 4% of the purchase price in concessions, which can include paying off debts for the buyer to qualify for the loan.

Considerations:

- Eligibility: Not everyone qualifies for a VA loan; you need to meet specific service requirements or be a surviving spouse of a veteran who died in service or from a service-connected disability.

- Funding Fee: While it’s not a prohibitive cost, the funding fee does add to the loan’s total amount unless you’re exempt.

VA loans are crafted to honor the service of military personnel by facilitating easier and more affordable home ownership. This suite of benefits makes the VA loan one of the most advantageous mortgage products available for eligible individuals. Remember, while the VA guarantees the loan, you still need to work with approved lenders who will have their criteria for loan approval.

FHA Loan Benefits: A Comprehensive Guide

FHA loans, insured by the Federal Housing Administration (FHA), are designed to make home ownership more accessible, particularly for those with lower credit scores or smaller down payments. Here are the key benefits of FHA loans:

1. Lower Down Payment Requirements

- Minimal Down Payment: FHA loans require as little as 3.5% down if your credit score is 580 or higher. If your score is between 500-579, you can still qualify with a 10% down payment. This low entry point is a significant advantage for first-time home-buyers or those with limited savings.

2. Flexible Credit Standards

- Lower Credit Thresholds: FHA loans are known for their more lenient credit score requirements. Borrowers with scores as low as 500 can potentially qualify, although rates might be higher for those with lower scores.

3. Gift Funds Allowed

- Down Payment Assistance: The down payment can often come from a gift, grant, or down payment assistance program, making it easier for buyers who might not have the cash on hand to purchase a home.

4. Competitive Interest Rates

- Favorable Rates: FHA loans often come with interest rates that are competitive with or better than conventional loans for borrowers with similar credit profiles, potentially saving money over the life of the loan.

5. Assumable Loans

- Loan Assumption: Like VA loans, FHA loans are assumable. This means if you sell your home, the buyer can take over your existing FHA loan, which could be advantageous if rates have risen since you took out your mortgage.

6. Easier to Qualify for Refinancing

- Streamline Refinance: FHA offers a streamline refinance program which requires less documentation and underwriting, making it simpler and sometimes cheaper to refinance your existing FHA loan to a lower rate or different term.

7. Fixed and Adjustable Rate Options

- Loan Variety: FHA loans come in both fixed-rate and adjustable-rate mortgage (ARM) options, providing flexibility based on your financial situation and plans.

8. Seller Contributions

- Selling Concessions: Sellers can contribute up to 6% of the sales price or appraised value toward the buyer’s closing costs, prepaids, and other related expenses, which can significantly reduce the out-of-pocket costs at closing.

9. Non-Occupying Co-Borrowers

- Family Support: FHA loans allow for a non-occupying co-borrower to help qualify for the loan, which can be beneficial if the primary borrower needs additional income or credit to qualify.

10. No Prepayment Penalties

- Prepayment Freedom: You can pay off your FHA loan early without any prepayment penalties, allowing you to save on interest if you decide to pay more than your monthly payment.

11. Broader Property Eligibility

- Various Property Types: FHA loans can finance single-family homes, multi-unit properties where the borrower will live in one unit, condos approved by HUD, and manufactured homes, providing diverse home buying options.

12. Mortgage Insurance Premium (MIP)

MIP Structure: While FHA loans require both an upfront and annual MIP, the structure allows for lower monthly payments due to the down payment flexibility. Also, after 11 years of payments, if you’ve put down at least 10%, you can request to have MIP removed.

Considerations:

- Mortgage Insurance: The necessity of paying mortgage insurance can be a downside for some, although it’s a trade-off for the lower down payment and easier qualification.

- Loan Limits: FHA loans have specific loan limits that vary by county, which could limit the purchase price in high-cost areas unless supplemented by other financing.

FHA loans are particularly beneficial for those looking to enter the housing market without substantial upfront capital or with credit challenges. They offer a viable path to home-ownership with benefits that cater to a wide range of buyers, especially first-time home buyers. However, as with any mortgage product, it’s crucial to understand the full terms, including the cost of mortgage insurance, and compare them against other loan options to ensure it’s the best fit for your financial situation.

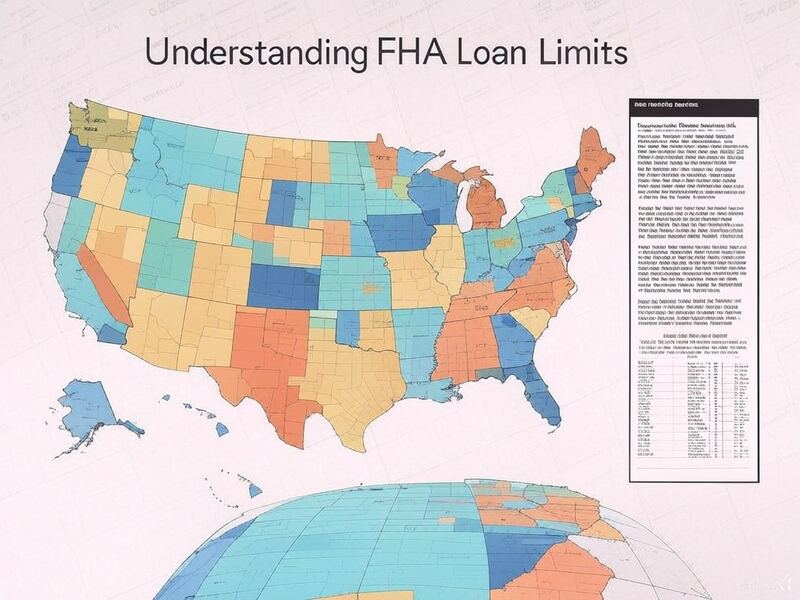

FHA Loan Limits: Understanding the Caps for 2025

FHA loan limits are established annually by the Federal Housing Administration (FHA) to dictate the maximum amount of money a borrower can secure through an FHA-insured mortgage. These limits are crucial as they influence how much a homebuyer can finance for their home purchase or refinance. Here’s a detailed look at FHA loan limits for 2025, keep checking on the current Fed rates as they can change.

Overview of FHA Loan Limits

Purpose: FHA loan limits help regulate the housing market by ensuring that the loans insured by the FHA are aligned with current home price valuations, ensuring affordability and responsible lending.

Annual Adjustment: Each year, FHA loan limits are adjusted based on the changes in median home prices across the U.S. These adjustments aim to reflect the economic conditions and housing market trends.

2025 FHA Loan Limits

Single-Family Homes (One-Unit Properties):

- Floor Limit: The “floor” limit for most areas in the U.S. for a single-family home is set at $524,225 for 2025.

- Ceiling Limit: In high-cost areas, the “ceiling” or maximum limit for a single-family home is set at $1,209,750.

Multi-Unit Properties:

- Two-Unit Properties: Low-cost areas have a limit of $671,200, while in high-cost areas, it’s $1,548,975.

- Three-Unit Properties: The limit is $811,275 in low-cost areas and $1,872,225 in high-cost areas.

- Four-Unit Properties: In low-cost areas, the limit is $1,008,300, and in high-cost areas, it’s $2,326,875.

- Special Exception Areas: In places like Alaska, Hawaii, Guam, and the U.S. Virgin Islands, due to higher construction costs, FHA limits are higher.

- One-Unit: $1,814,625

- Two-Unit: $2,323,463

- Three-Unit: $2,808,338

- Four-Unit: $3,490,300

How FHA Loan Limits are Determined

- Conforming Loan Limits: FHA loan limits are based on a percentage of the conforming loan limits set by the Federal Housing Finance Agency (FHFA) for conventional loans. For 2025, the conforming loan limit for a one-unit property in most areas is $806,500.

- Median Home Prices: The FHA looks at median home prices in each county or metropolitan statistical area (MSA). If a county’s median home price exceeds 115% of the floor limit, the FHA adjusts its loan limit accordingly.

- Floor and Ceiling: The floor is 65% of the conforming loan limit, and the ceiling is 150% for high-cost areas.

Implications for Borrowers

- Access to Higher Priced Homes: Higher FHA loan limits in expensive areas mean more potential homebuyers can use FHA financing for homes in those markets.

- Jumbo FHA Loans: When the loan amount exceeds the standard FHA limit but is below the ceiling, it’s considered a “jumbo” FHA loan. These loans are available where housing costs are significantly above average.

- Refinancing: FHA loan limits also apply to refinancing, ensuring that borrowers can refinance up to the current year’s limits.

- Property Type Impact: Multi-unit properties have higher limits, which can encourage investment in rental properties alongside primary residence ownership.

How to Check Your Local Limits

HUD Website: The U.S. Department of Housing and Urban Development (HUD) provides an online tool where you can look up the FHA loan limits by county or state.

Lender Guidance: Most lenders also have this information readily available, often on their websites, or they can provide it upon request.

FHA loan limits for 2025 reflect a response to the current housing market conditions, aiming to balance home affordability with the realities of rising home prices. These limits are essential for prospective homeowners to understand as they navigate the mortgage landscape, ensuring they can plan their home purchase within the confines of what FHA-insured financing allows. Remember, while these limits set the cap on borrowing, individual approval still depends on creditworthiness, income, and other financial factors.

FHA Loan Eligibility: Who Qualifies for an FHA Loan?

FHA loans, backed by the Federal Housing Administration, are designed to make home ownership more accessible to a broader audience, including first-time buyers, those with lower credit scores, or those without substantial savings for a down payment. Here’s a detailed breakdown of the eligibility criteria for obtaining an FHA loan:

Basic Eligibility Requirements

Credit Score:

Minimum Credit Score: The FHA doesn’t specify a minimum credit score, but most lenders require at least a 500 FICO score. For a 3.5% down payment, a score of 580 or higher is typically needed. If your score is between 500-579, you might still qualify but with a 10% down payment.

Down Payment:

3.5% Down Payment: If your credit score is 580 or above, you can secure an FHA loan with just 3.5% down.

10% Down Payment: For scores between 500-579, a 10% down payment is required.

Debt-to-Income Ratio (DTI):

Standard DTI: Typically, your front-end DTI (housing costs vs. income) should not exceed 31%, and back-end DTI (total debt vs. income) should be under 43%. However, higher ratios can sometimes be approved based on compensating factors like a larger down payment or stable employment history.

Property Eligibility:

Primary Residence: The property must be your primary residence. FHA loans can finance single-family homes, multi-family units (up to 4 units with one unit owner-occupied), condos, and manufactured homes that meet FHA guidelines.

Loan Limits:

Adherence to Limits: Your loan amount must be within the FHA loan limits for your area, which vary by county.

Additional Eligibility Considerations

Income:

Stable Income: You need to demonstrate steady employment or income to show you can afford the mortgage payments. This includes wages, self-employment income, and even non-taxable income like child support or Social Security.

Employment History:

Job Stability: While there’s no set minimum time period, lenders look for stability in employment, often preferring two years with the same employer or in the same line of work.

Credit History:

- Credit Events: Bankruptcies, foreclosures, and other significant credit issues don’t automatically disqualify you but must have passed certain waiting periods:

- Chapter 7 Bankruptcy: Typically, 2 years from discharge.

- Chapter 13 Bankruptcy: During or after discharge, with court permission if still in repayment.

- Foreclosure: Usually, 3 years from the foreclosure date unless there are extenuating circumstances.

- Short Sale: 3 years, with possible exceptions for certain circumstances.

Legal Residency:

- U.S. Citizenship or Legal Residency: You must be a U.S. citizen, permanent resident, or have a valid visa with proof of work authorization.

Funds for Closing Costs:

- Closing Costs: While the down payment can be low, you’ll need funds for closing costs unless you’re using a program that covers these or negotiating seller concessions.

Special Programs and Considerations

Down Payment Assistance: Many states and local programs offer down payment assistance specifically for FHA loans, which can further reduce the initial cash needed.

FHA 203(k) Loans: For those buying homes needing repairs, the FHA 203(k) program allows you to finance both the purchase and rehabilitation of a property.

Non-Occupant Co-Borrowers: This feature allows someone not living in the home to co-sign the loan, potentially helping with qualification based on their income.

Manual Underwriting: If your automated underwriting doesn’t approve you, manual underwriting might be an option where a human underwriter reviews your entire financial profile, potentially approving you with compensating factors.

How to Apply for an FHA Loan

- Lender Selection: Choose an FHA-approved lender. Not all lenders offer FHA loans.

- Pre-Approval: Get pre-approved to understand how much home you can afford.

- Application: Submit your application with required documentation like income verification, credit reports, and more.

- Underwriting: Await the underwriting process where your loan is evaluated.

- Closing: If approved, proceed to closing where you’ll sign all documents and finalize your mortgage.

Understanding FHA loan eligibility can open doors to home ownership for many who might find conventional mortgage criteria too restrictive. However, while FHA loans provide more flexible entry points, they also require an understanding of their ongoing costs, like mortgage insurance premiums (MIP), which are mandatory for the life of the loan if you put down less than 10%. Always consider speaking with an FHA loan expert or financial advisor to navigate your specific situation and explore all available options.

Credit Score Requirements for Different Types of Loans

Credit scores play a pivotal role in determining loan eligibility and the terms you will receive. Here’s an overview of credit score requirements for various types of mortgages:

Conventional Loans

General Requirement:

- Minimum Score: Typically, a minimum score of 620 is required by many lenders for conventional loans. However, some might go lower with certain programs.

- Best Rates: To secure the best interest rates, a score of 740 or higher is often needed.

Loan-to-Value (LTV) Ratio:

- Lower credit scores might require a higher down payment to reduce the LTV ratio, thus lowering risk for the lender.

PMI (Private Mortgage Insurance):

- If your down payment is less than 20%, PMI is required unless you qualify for certain programs or have compensating factors.

FHA Loans

Minimum Credit Score:

- 3.5% Down Payment: A score of 580 or above allows for a 3.5% down payment.

- 10% Down Payment: If your score is between 500-579, you can still qualify but with a 10% down payment.

MIP (Mortgage Insurance Premium):

- All FHA loans require MIP, which is part of the trade-off for lower credit score requirements.

VA Loans

No Set Minimum Credit Score from VA

- Lender Standards: While the VA itself does not specify a minimum credit score, lenders will have their own criteria. Commonly, a score of 620 or higher is preferred,

but some might approve loans with scores in the 500s if there are compensating factors like low debt-to-income ratio or significant assets. - No Down Payment: VA loans are attractive for their no down payment requirement, making them accessible to those with lower credit scores.

USDA Loans

Rural Development Loans

- Minimum Score: The USDA doesn’t set a minimum credit score, but lenders typically look for at least 640. Some might approve with lower scores if the applicant has strong compensating factors.

- No Down Payment: Like VA loans, USDA loans offer zero down payment, aimed at rural or suburban home buyers.

Jumbo Loans

Higher Scores Required

- Minimum Score: Jumbo loans often require a credit score of 700 or higher due to the larger loan amounts involved. Some might require 720 or above for the best rates.

- Stricter Criteria: Given the higher risk, lenders might also require a lower debt-to-income ratio, larger down payment, and more reserves.

Other Considerations

Manual Underwriting: For those with lower scores or unique financial situations, some loans can be manually underwritten, where a human underwriter evaluates the entire financial picture, not just the credit score.

Credit History: Beyond the score, lenders look at:

- Payment history

- Length of credit history

- Types of credit used

- Amounts owed

- New credit inquiries

Improving Your Credit Score: If your score is below the threshold for your desired loan type:

- Pay bills on time

- Reduce outstanding debt

- Avoid new credit applications before buying

- Dispute errors on your credit report

- Keep old accounts open to maintain a long credit history

Alternative Credit Data: Some lenders might consider alternative data like rent or utility payment history for those with thin credit files.

While credit score requirements can seem daunting, they are just one part of the home loan equation. Lenders also assess income, employment history, debt levels, and other financial factors. If you’re below the typical score thresholds, there are still options:

- Credit Building: Work on improving your credit over time.

- Co-signers: If you have a co-signer with a good credit score, this can sometimes compensate for your lower score.

- Special Programs: Look for government or local programs aimed at helping those with lower credit scores.

Remember, each lender might have slight variations in their criteria, so shopping around and discussing your situation with multiple lenders can be beneficial.

FHA Loan Down Payments: A Comprehensive Guide

FHA loans, insured by the Federal Housing Administration, are known for their more accessible down payment requirements, making home ownership possible for those with limited savings or lower credit scores. Here’s an in-depth look at the down payment requirements for FHA loans:

Standard Down Payment Requirements

Credit Score 580 and Above:

- 3.5% Down Payment: If your credit score is 580 or higher, you can qualify for an FHA loan with just a 3.5% down payment. For a $300,000 home, this would mean a down payment of $10,500.

- Credit Score Between 500 – 579:

- 10% Down Payment: Borrowers with credit scores in this range need to put down at least 10%. Using the same $300,000 home example, that’s $30,000 down.

Down Payment Sources

- Personal Funds: Money from your savings or checking accounts.

- Gifts: Down payments can come entirely from gifts, provided the gift is from an acceptable source like family members, employers, or certain charitable organizations. There’s no limit on the amount of gift funds as long as they’re documented correctly.

- Grants and Assistance Programs: Many states and local governments offer down payment assistance programs specifically for FHA loans. These can be in the form of grants, second mortgages, or forgiven loans over time.

- Seller Concessions: Sellers can contribute up to 6% of the home’s sales price towards your closing costs, which indirectly helps manage down payment funds.

Down Payment Considerations

- No Cash Reserves Required: Unlike some conventional loans where significant cash reserves might be required, FHA loans do not mandate this, making them more feasible for those with minimal savings beyond the down payment.

Mortgage Insurance:

Upfront Mortgage Insurance Premium (UFMIP): You’ll pay 1.75% of the loan amount at closing or finance it into the loan. For a $300,000 loan, that’s an additional $5,250.

Annual Mortgage Insurance Premium (MIP): An ongoing cost, currently at rates between 0.45% to 1.05% of the loan annually, depending on the loan term and LTV. This is usually paid monthly but can be paid annually if preferred.

Property Condition: If you’re buying a home needing repairs, consider the FHA 203(k) loan, which allows you to include the cost of repairs in your loan amount, potentially offsetting part of what you’d need for a traditional down payment.

Down Payment Strategies

- Save Over Time: Even if you’re eligible for a low down payment, saving more can reduce your loan amount and monthly payments.

- Down Payment Assistance: Research local, state, or national programs. Some are tailored for first-time home buyers or specific demographics like veterans or teachers.

Gift Letters: If relying on gifts, ensure you have a gift letter stating no repayment is expected and the source of funds.

Seller Contributions: Negotiate with the seller for concessions to help with closing costs, freeing up your cash for the down payment.

Down Payment Exceptions -FHA Loan

FHA Streamline Refinance: For those refinancing an existing FHA loan, no down payment or appraisal is typically required, but you must be current on your mortgage.

FHA 203(k): While you still need a down payment, this loan allows you to finance the purchase and the cost of repairs/improvements into one loan, potentially reducing upfront costs.

Conclusion

FHA loans provide a pathway to home ownership with down payment requirements that are lower than many conventional loans, making them an attractive option for many. However, the trade-off includes mortgage insurance premiums, which add to the cost of home ownership.

Prospective buyers should weigh these factors, explore all down payment assistance options available, and perhaps consult with a mortgage professional to understand how an FHA loan fits into their broader financial picture.

Remember, while the down payment might be lower, other costs like closing costs, insurance, and maintenance should also be budgeted for when planning to buy a home.

> Recommended: brokerage for trading > tastytrade.com.

> Recommended: order flow heatmap > bookmap.com.